How Much of Moving Expenses Are Tax Deductible? What Are Allowable Moving Expenses?

Moving Expenses

Certain individuals may be able to exclude from income the value of services and reimbursements received from an employer for moving expenses. If they are not reimbursed, they may be able to deduct expenses incurred when they moved.

Limitation

For tax years through 2025, the moving expense deduction and the exclusion from gross income and wages for qualified moving expense reimbursements have been suspended and are not available for most taxpayers.

Exception: Active duty servicemembers of the Armed Forces (and their spouses and dependents) moving under military orders and incident to a permanent change of station can continue to claim the moving expense deduction and receive excludable moving expense reimbursements.

The exclusion applies only to reimbursement of moving expenses that the servicemember could deduct if he or she had paid or incurred them without reimbursement.

Deductibility Tests

Servicemembers of the Armed Forces can deduct moving expenses without meeting a time or distance test if both of the following criteria are satisfied.

- You are on active duty.

- You move because of a permanent change of station.

Permanent Change Of Station (PCS).A permanent change of station includes:

- A move from your home to your first post of active duty,

- A move from one permanent post of duty to another, and

- A move from your last post of duty to your home or to a nearer point in the United States. The move must occur within one year of ending your active duty or within the period allowed under the Joint Travel Regulations.

Other Circumstances. If you are the spouse or dependent of a servicemember of the Armed Forces who deserts, is imprisoned, or dies, a permanent change of station for you includes a move to:

- The servicemember’s place of enlistment or induction,

- Your, or the servicemember’s, home of record, or

- A nearer point in the United States.

If the military moves you to or from a different location than the servicemember, the moves are treated as a single move to your new main job location.

Foreign Moves

A foreign move is a move from the United States or its possessions to a foreign country or from one foreign country to another foreign country. A move from a foreign country to the United States or its possessions is not a foreign move. For a foreign move, the deductible moving expenses, described later, are expanded to include the reasonable expenses of:

- Moving household goods and personal effects to and from storage, and

- Storing these items for part or all of the time the new job location remains the servicemember’s main job location. The new job location must be outside the United States.

Deductible Moving Expenses

- The cost of transportation and storage (up to 30 days after the move) of household goods and personal effects.

- Travel, including lodging, from the old home to the new home. Travel is limited to one trip per person. However, each member of the household can move separately and at separate times. If the taxpayer drives his or her own vehicle, expenses can be figured either using actual out-of pocket expenses for gas and oil (but not depreciation), or the standard mileage rate for moving (for 2021, 16¢ per mile), plus parking fees and tolls.

Not Deductible. Cost of meals while traveling, temporary living expenses, lavish or extravagant lodging, or house hunting expenses before or after the move.

Governmental Provided Moving Services And Allowances.

Nondeductible expenses include:

- Moving services provided by the government.

- Reimbursements by an allowance not included in the servicemember’s income.

Nondeductible Expenses

The following expenses are not deductible as moving expenses.

- Any part of the purchase price of a new home.

- Car tags or driver’s license.

- Expenses of entering into or breaking a lease.

- Loss on home sale.

- Mortgage penalties

- Pre-move house hunting trips.

- Real estate taxes.

- Security deposits.

Reimbursed Moving Expenses

Eligible moving expenses reimbursed by the government are excluded from your taxable wages. The amount of excluded moving expenses is reported in box 12, Form W-2 under code “P.” Do not deduct any expenses for moving services that were provided by the government. Also, do not deduct any expenses that were reimbursed by an allowance not included in income.Additional moving expenses that are not reimbursed are eligible for a deduction on Schedule 1 (Form 1040) if they otherwise qualify.

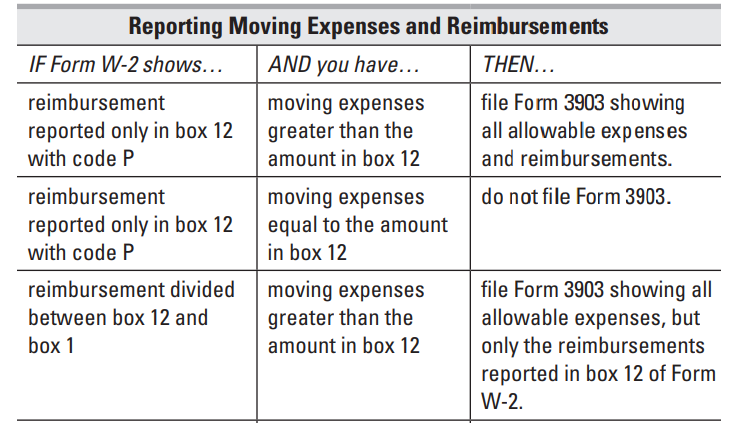

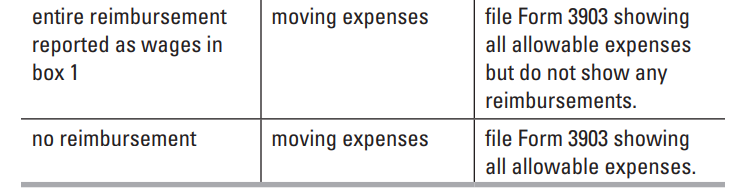

Form 3903, Moving Expenses

The moving expense deduction is computed on Form 3903. See the Reporting Moving Expenses and Reimbursements chart, next column, to determine how to figure the deduction for qualified expenses that exceed reimbursements and allowances (including dislocation, temporary lodging, temporary lodging expense, or move-in housing allowances that are excluded from gross income). The moving expense deduction is carried from Form 3903 to line 13, Schedule 1 (Form 1040), as an adjustment to income. If you do not have any out-of-pocket unreimbursed moving expenses, there is no moving expense deduction allowed.