What Triggers the Alternative Minimum Tax? Who Is Subject to Alternative Minimum Tax? How Do I Avoid Alternative Minimum Tax?

Alternative Minimum Tax (AMT)

The alternative minimum tax was originally enacted to ensure that high-income taxpayers pay at least a minimum amount of tax if they benefit from certain deductions and other tax preference items.

The AMT tax computation is a parallel system to the regular tax system with its own definitions of income and expenses, rules for income recognition and timing, exemptions, and tax rates. Although every taxpayer is subject to AMT rules, the additional tax is paid only if the tax computation under AMT rules is higher than the tax computed under regular rules.

Even though the AMT was originally targeted toward high-income taxpayers, factors, including inflation and treatment of certain tax credits, can sometimes push lower-income taxpayers into an AMT situation.

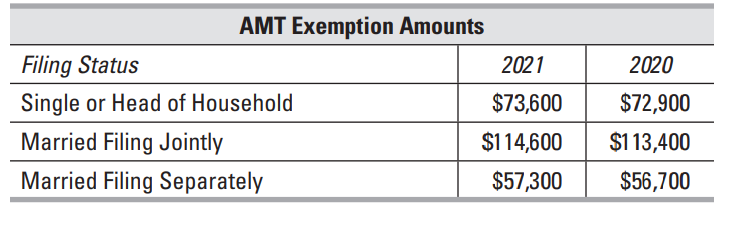

How AMT Works

Certain items called adjustments and preferences are added to or subtracted from federal adjusted gross income reduced by any itemized deductions. An AMT exemption amount is allowed, depending on the taxpayer’s filing status. The AMT tax rate of 26% to 28% is applied to the resulting alternative minimum taxable income. If the resulting tax is greater than regular tax, the difference is added to regular tax on Form 1040.

Example #1: When computed under regular rules, John’s income tax is $4,700. When computed under AMT rules, the tax amount is $3,900. Since his tax computed under AMT rules is less than his tax computed under regular rules, John will not pay any additional amount for AMT.

Example #2: Assume the same facts as Example #1, except when computed under AMT rules, John’s tax amount is $5,100. Since his tax computed under AMT rules is higher than his tax computed under regular rules, John must pay the difference in additional tax. John must report additional AMT tax in the amount of $400.

AMT Triggers

Items that commonly trigger AMT include deductions for state and local taxes, and exercise of incentive stock options. Other AMT adjustments and preferences include:

- Taxes from Schedule A (Form 1040).

- Tax refunds reported on Form 1040.

- Certain investment interest expense.

- Certain depletion expenses.

- Net operating losses.

- Interest from specified private activity bonds.

- A portion of gain from section 1202 small business stock.

- Exercise of incentive stock options.

- Certain gains from dispositions of property.

- Certain depreciation adjustments.

- Passive activity gains and losses.

- AMT loss limitations.

- Certain circulation costs.

- Long-term contracts.

- Certain mining costs.

- Certain research and experimental costs.

- Pre-1987 installment sale income.

- Intangible drilling cost preferences.

Incentive Stock Options—amt Adjustments

The bargain element resulting from exercise of incentive stock options (ISO) is equal to the fair market value (FMV) of the stock minus the exercise price and is a deferral item for AMT purposes.

Form 3921, Exercise of an Incentive Stock Option Under Section 422(b), may help in computing the adjustment.

Example: Cindy exercised an ISO to acquire 100 shares of stock in 2021. Her rights in the acquired stock first became transferable on the date she exercised the ISO and were not subject to a substantial risk of forfeiture. She did not pay anything for the ISO and did not sell the acquired stock during 2020.

Cindy received Form 3921 that shows $10 in box 3 (the exercise price paid for each share), $25 in box 4 (the fair market value of each share on the exercise date), and 100 shares in box 5 (the number of shares acquired). To calculate the adjustment, multiply the amount in box 4, $25, by the 100 shares in box 5. The result is $2,500, the fair market value of all the shares. Then multiply the amount in box 3, $10, by the 100 shares in box 5. The result is $1,000, the amount paid for all the shares.

Cindy’s AMT adjustment is $1,500 ($2,500 − $1,000).

Potential Tax Credit. If the AMT adjustment due to exercise of an ISO results in an AMT liability, an AMT credit may be available in subsequent tax years.

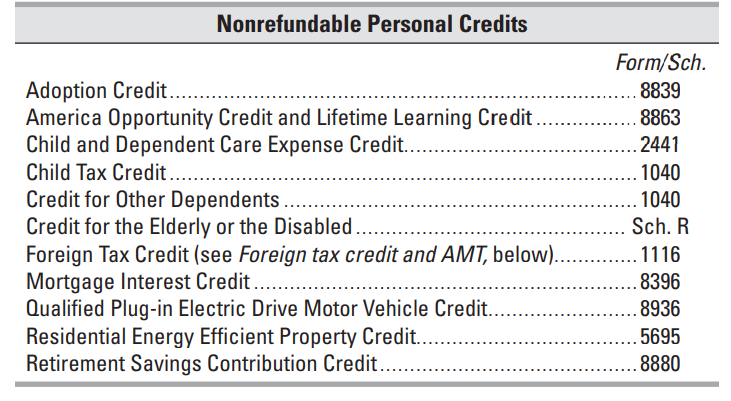

Personal Credits

An individual can claim nonrefundable personal credits against regular tax and AMT.

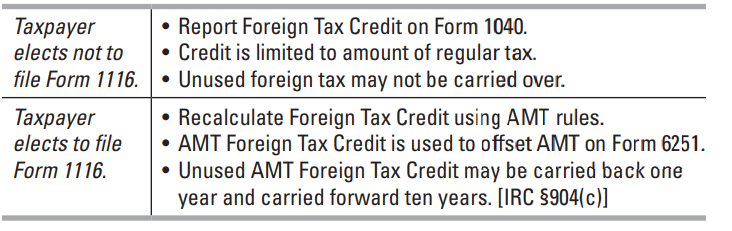

Foreign Tax Credit And AMT

The AMT treatment of the Foreign Tax Credit depends on whether Form 1116, Foreign Tax Credit, is being filed.

Credit For Prior Year AMT

The adjustments and preferences that result in AMT are of two types.

1) Deferral items, such as AMT basis adjustments, are temporary and do not cause a permanent difference in taxable income over time.

2) Exclusion items, such as taxes from Schedule A (Form 1040), are not allowed for AMT and therefore cause a permanent difference in taxable income.

The potential exists for income from deferral items to be taxed twice—first under AMT, and again in a later year under regular tax. A credit against regular tax for prior year AMT is available to address this situation.