How Are Stock Options Taxed When Sold? Do You Pay Taxes Twice on Stock Options? How Do You Avoid Tax on Stock Options?

Employee Stock Options

A stock option allows (but does not obligate) an employee to buy a specified number of shares of stock from a company for a specified price during a specified period of time. There are two categories of stock options.

- Nonstatutory (nonqualified) stock options.

- Statutory (qualified) stock options. Statutory stock options include incentive stock options (ISOs) and employee stock purchase plan options (ESPPs).

The employer determines the type of option offered to an employee.

The term “nonqualified stock option” is a technical term describing certain types of stock options granted to employees. The term refers to how the gain is taxed, not to the legitimacy of the transaction.

Qualified Stock Options

Qualified stock option plans offer tax advantages and must comply with specific IRS rules. For most qualified stock option plans, you must actually purchase the stock and hold it for at least one year before selling, after which time any gain on the sale is subject to favorable capital gain tax rates.

Nonqualified Stock Options

Nonqualified stock options have fewer restrictions than qualified stock option plans. If you purchase stock at a discount under a nonqualified stock option plan, the bargain element (the difference between the option price and market value) is taxable to you as wages at the time the option is exercised.

Same Day Sales

When an employer grants a stock option to you, you are often eligible for a same-day sale, allowing you to simultaneously exercise the option and sell the stock. In a same-day sale, you are not required to pay for the stock up front, but you receive cash in the amount of the difference between the exercise price and the value of the stock.

Example: Diamond, Inc. grants its employee, Dennis, a stock option to purchase company stock for $17,000. The stock is worth $25,000. Dennis chooses to cash it out in a same-day sale. Even though he was not required to provide any payment up front, the transaction is treated as if Dennis paid $17,000 for the stock and sold it for $25,000. Dennis reports the stock sale on his return and Diamond, Inc. includes $8,000 ($25,000 – $17,000) as additional compensation on Dennis’ Form W-2.

Taxation Of A Same-day Sale

Because of an unusual quirk in reporting for a same-day stock sale, the proceeds are reported to you twice—once as taxable wages on Form W-2, Wage and Tax Statement, and again as proceeds from a stock transaction on Form 1099-B, Proceeds from Broker and Barter Exchanges Transactions. Every year, taxpayers get bills for a balance due from the IRS because they did not properly report proceeds and basis from stock options in addition to their income on Form W-2.

Form W-2

The “bargain element,” which is the difference between the exercise price and the stock value, is taxable to you as wages and subject to federal and state withholding. The bargain element is included in box 1 of your Form W-2, and is included in wages on line 1, Form 1040. Since the amount is already included in taxable wages, no additional steps need to be taken to report the bargain element on your tax return.

Code “V”

Box 12 of Form W-2 should show code “V,” which reports income from exercise of nonstatutory stock options. This amount is already included as taxable wages in box 1. The amount listed under code “V” is informational, and is not required to be added to income.

In the Diamond, Inc. example in the previous page, the amount of taxable wages in box 1 of Form W-2 will increase by $8,000, and $8,000 is reported in box 12, code “V.”

Form 1099-B

Even though the income from the same-day transaction has already been included in wage income on Form 1040, because this was a broker transaction you will also receive Form 1099-B showing total proceeds from a stock sale. Since the 1099-B shows only the total sales price of the stock, and does not always indicate gain or loss, the transaction must be properly reported to avoid double taxation.

In the Diamond, Inc. example in the previous page, Dennis receives Form 1099-B showing proceeds from stock sales of $25,000. If he does not properly report the transaction, the IRS will assume he had a gain of $25,000 that was not reported on his tax return, and will send him a bill for the balance due.

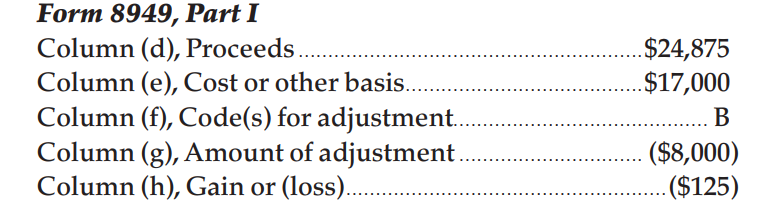

Form 8949, Sales And Other Dispositions Of Capital Assets

Proceeds from a same-day transaction are reported on Form 8949, Sales and Other Dispositions of Capital Assets. Form 8949 is where your tax basis is reported which results in gain or loss from the sale of stock. Proper reporting of a same-day sale on Form 8949 will generally result in a loss equal to brokers fees and commissions, although it is possible to show a small gain because of fluctuations of the stock price on the day of the sale.

Form 8949

If you sell stock or any other capital asset you must file Form 8949. The form lists each transaction by type and totals are carried to Schedule D (Form 1040). Use Form 8949 to report the following transactions.

- Transactions reported on Form 1099-B, see below.

- The sale or exchange of a capital asset not reported on another form or schedule.

- Gains from involuntary conversions (other than from casualty or theft) of capital assets not held for business or profit.

- Non-business bad debts.

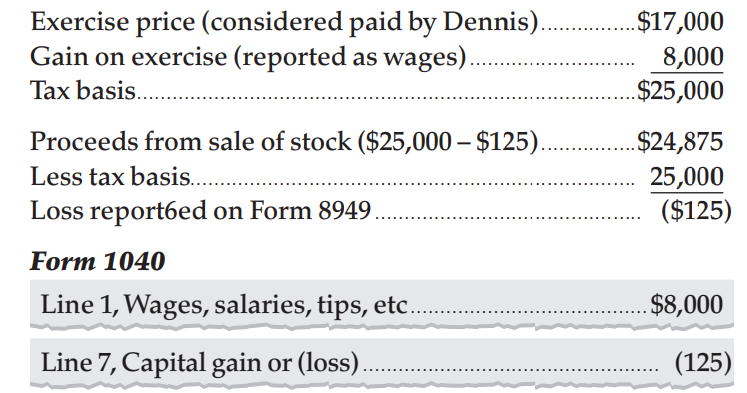

Example: Dennis has reported $8,000 income from a same day stock sale as wages on his Form 1040. He also received Form 1099-B showing proceeds from the stock sale of $24,875 ($25,000 – $125 broker fees). Dennis is computing his tax basis to determine gain or loss to report on Form 8949. His tax basis is computed as follows.