What Is a Compensation Package Example? What Is an Effective Compensation Plan? What Is an Example of Compensation?

Deferred Compensation Plans

Deferred-compensation plans let employees defer salary or bonus to a future year. The plan may credit the employee with earnings that grow tax deferred. To obtain tax deferral, a deferred-compensation plan must be:

- Unfunded or

- Subject to a substantial risk of forfeiture (that is, unvested).

Two pitfalls that must be avoided to ensure tax deferral are:

- Constructive Receipt. Income is constructively received in the year made available without restrictions to the employee—but not if substantial restrictions exist on the employee’s right to the deferred pay.

- Economic Benefit Doctrine. Income is recognized when an employee acquires a nonforfeitable right to employer assets that supersedes the rights of general creditors.

Tougher Rules Under Section 409A. Section 409A adds a set of rules that make it more difficult for employees to defer compensation for tax. If applicable, the rules generally require deferred compensation elections to be made before the beginning of the year in which the related compensation will be earned.

Restricted Stock

A restricted stock plan is an arrangement where an employee receives company stock (often at little or no cost) subject to certain restrictions. An employee who fails to fulfill the terms of the restricted stock program forfeits the restricted shares.

section 83(b) election. Generally, income is not recognized when an employee receives restricted stock. However, employees can elect to recognize compensation income at the date of receipt. The amount included in income is the excess of the stock’s value upon receipt over the amount, if any, the employee paid for the stock. A Section 83(b) election may be beneficial when:

- The shares have nominal value at the transfer date.

- The employee pays full or substantial value for the stock.

- Significant stock value appreciation is likely between the date of receipt and when the stock substantially vests.

Stock-Based Compensation

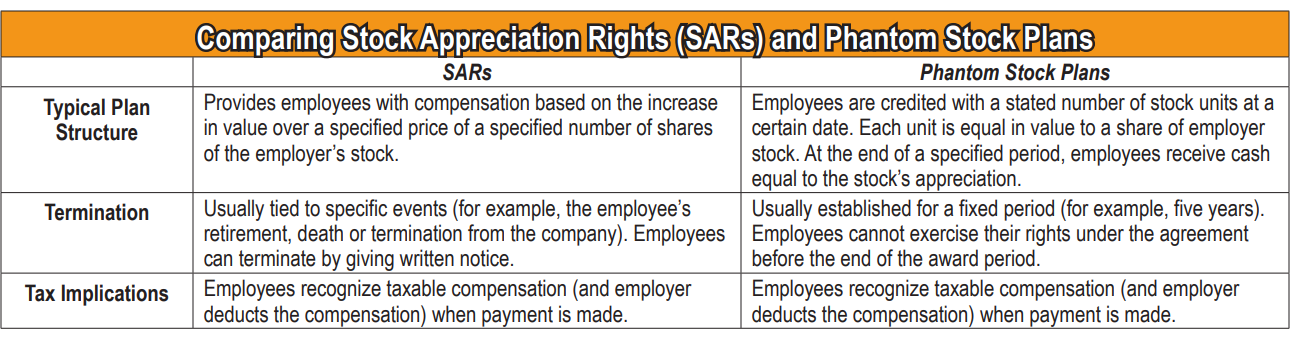

Stock appreciation rights (SARs) and phantom stock plans base a portion of the employee’s cash compensation on the value of the employer’s stock. This links monetary rewards with the stock price without actually transferring shares to the employee.

Employer Stock Options

A stock option is a contractual right granted an employee to purchase shares of the company’s stock. The plan normally specifies how many options may be granted, who may participate, the option price, the form of payment, the periods for exercising options and making payment, and other matters.

Stock Option Terminology

Grant Date

The date on which an employee receives an option.

Exercise Date

The date the employee exercises the option to buy stock.

Option Price

The price at which the stock can be purchased under the terms of the option. Also called the exercise price or the strike price.

Bargain Element

The difference between the fair market value (FMV) of the stock and the option price of an inthe-money option.

Even-Money

When the option price equals the stock’s FMV. In-the-Money When the option price is less than the stock’s FMV.

Incentive Stock Options (ISOs)

Must meet certain requirements to qualify. Generally, an ISO benefits the employee because any appreciation after the exercise date is taxed as long-term capital gain if holding periods are met.

Nonqualified Stock Options (NQSOs)

Generally more flexible than ISOs. NQSOs generally create compensation income for the employee and an offsetting deduction for the employer upon exercise.

Funding The Exercise Price Of Options:

- Cash Payment. Employees uses available cash.

- Leverage. Borrowing money to fund exercise prices minimizes out-of-pocket costs. Interest paid on loan is generally deductible.

- Cashless. Employee borrows funds needed to exercise options from a broker and immediately sells option shares to repay the loan. Employees avoids any out-of-pocket cost to exercise.

- Exchanging Old Shares. Employee trades in shares already owned to pay exercise price. The exchange is nontaxable.

Tax Implications Of Isos:

- Neither grant nor exercise of an ISO creates compensation income to employees, but employees may have an alternative minimum tax (AMT) adjustment upon exercise.

- Exercise price becomes the employee's basis in acquired stock.

- Employees recognize income or loss when stock acquired through option exercise is disposed of.

- Character of income (ordinary versus capital gain) from sale of ISO shares depends on whether stock is held at least one year and ISO granted at least two years before disposition. If holding period rules are not met, sale is a disqualifying disposition, with gain allocated between ordinary income and capital gain.