How Do You Reduce Individual Taxes? What Is Individual Taxation?

Other Individual Taxes

3.8% Net Investment Income Tax

Individuals are subject to a net investment income tax equal to 3.8% of the lesser of:

1) Net investment income (NII) or

2) The excess (if any) of adjusted gross income (AGI) over the threshold amount.

Net Investment Income

NII is the sum of the following, reduced by allowable deductions:

1) Gross income from interest, dividends, annuities, royalties, and rents, unless they are derived in the ordinary course of a trade or business that is not a passive activity.

2) Other gross income derived from a trade or business that is a passive activity.

3) Net gain attributable to the disposition of property other than property that is not subject to the NII tax.

Note: A passive activity is a trade or business in which the individual does not materially participate. Usually, an individual must work in the business more than 500 hours during the year to materially participate.

Additional Medicare Tax

Wages, compensation and self-employment (SE) income are subject to the 0.9% additional Medicare tax to the extent they exceed the following thresholds.

Note: Any additional Medicare tax paid by self employed individuals does not qualify for the deduction for one half of SE tax.

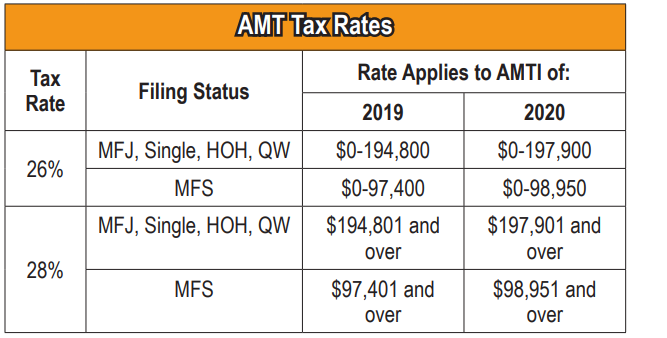

Alternative Minimum Tax

Individuals must compute their income tax under both the regular income tax and the alternative minimum tax (AMT) rules. They pay the greater of the two amounts.

To arrive at alternative minimum taxable income (AMTI), taxable income under the regular tax rules is adjusted for adjustments and exclusions. Then an AMT exemption amount is subtracted. The AMT exemption amount phases out at higher levels of AMTI.

AMT Adjustments And Preferences AMT Adjustment Items

Usually require separate AMT computations and are substituted for the amounts computed for regular tax purposes. These can result in either positive or negative adjustments to regular taxable income in arriving at AMTI.

AMT Preference Items result in amounts added back to regular taxable income to arrive at AMTI. Adjustments and preferences that merely change the timing of when an item is recognized are deferral items. Items that cause a permanent difference between regular and AMT taxable income are exclusion items.

Common AMT Adjustments And Preferences Deferral Items:

- Depreciation.

- Exercise of incentive stock options (ISOs).

- Gains or losses on disposition of property.

- Intangible drilling costs (IDC).

- Passive activities.

Exclusion Items:

- Gain from sale of qualified small business stock.

- Interest income from private activity bonds. Does not include interest on bonds issued in 2009 or 2010.

- Itemized deductions:

–Medical expenses over 7.5%.

–Miscellaneous deductions, 2017 only.

–Mortgage interest not used to buy, build or improve a home.

–Mortgage interest on a second home that is a boat or RV.

–Property taxes.

–State and local income or general sales taxes.

- Personal exemptions, 2017 only.

- Standard deduction.

- Tax refunds.