Can I Claim My Laptop as an Education Expense? Is It Better to Claim College Student as Dependent? Do I Need Receipts for Education Expenses?

Education Tax Benefits

If you pay tuition, fees, and other costs for attendance at an eligible educational institution for yourself, your spouse, or your dependent, you may be able to take advantage of one or more of the education tax benefits.

You can claim more than one education benefit in a tax year as long as you do not use the same expenses for more than one benefit.

Exception: Qualified expenses used to claim education benefits can also be used to eliminate the 10% penalty on premature IRA distributions.

For each student, you can elect for any year only one of the following benefits. For example, if you elect to claim the American Opportunity Credit for the student in 2021, you cannot use that same student’s qualified education expenses to compute the Lifetime Learning Credit or tuition and fees deduction.

Education Deductions

Deductions reduce the amount of income subject to income tax. Deductions for education expenses include:

- Student loan interest deduction up to $2,500 from gross income. Income limitations apply.

- Business deduction on Schedule C or F. You may be able to deduct the cost of education related to the business or farm activity.

Education Tax Credits

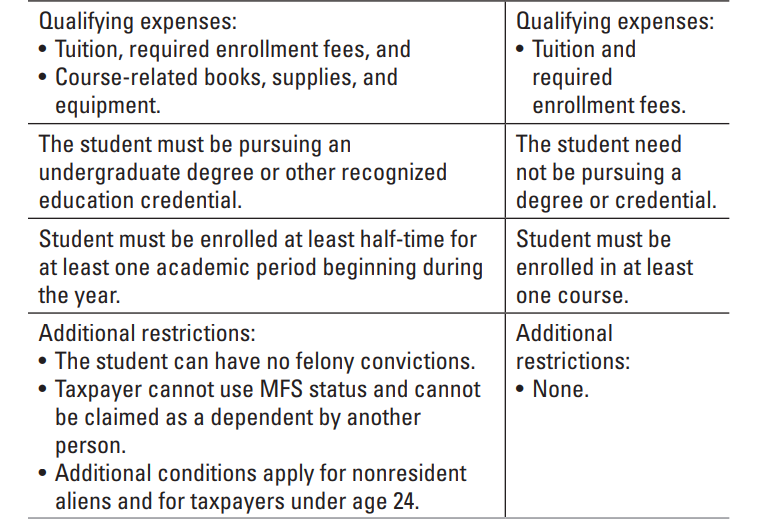

Tax credits reduce the amount of income tax you may have to pay. Income limitations apply. The education credits are claimed on Form 8863, Education Credits (American Opportunity and Lifetime Learning Credits).

- American Opportunity Credit, $2,500 maximum per student per year.

- Lifetime Learning Credit, $2,000 maximum per tax return per year.

Income Limits

The American Opportunity Credit is phased out at modified AGI between $80,000 and $90,000 ($160,000 and $180,000 MFJ) in 2021.

The Lifetime Learning Credit is phased out at modified AGI between $80,000 and $90,000 ($160,000 and $180,000 MFJ) in 2021.

Penalty-free IRA Distributions

If you withdraw money from your IRA before you are age 59½, you are generally subject to a penalty of 10% of the distribution, in addition to any tax that may be due on the distribution.

- The 10% penalty does not apply to traditional IRA or Roth IRA withdrawals, if you use the money to pay qualified education expenses for yourself, spouse, or for any child or grandchild of yourself or your spouse.

- Qualified education expenses include tuition, fees, books, supplies, equipment, and special needs services required for enrollment or attendance at an eligible educational institution. Room and board for students enrolled at least half-time in a degree or certificate program may also qualify.

- Reduce qualified expenses by scholarships and other tax free assistance the student receives, but not by gifts or inheritances.

Education Savings Plans

Contributions that you make to education savings plans are not federally tax deductible, but the earnings accumulate tax free. In addition, no tax will be owed on distributions if they are less than the beneficiary’s qualified education expenses. Qualified expenses are reduced by scholarships, other tax-free assistance, and amounts used to figure education credits.

- Qualified Tuition Programs (QTPs). States sponsor QTPs to allow prepayment of a student’s qualified higher education expenses. For information on a specific QTP, you need to contact the state agency or eligible educational institution that established and maintains it. You may not distribute more than $10,000 in expenses for tuition during the taxable year for a public, private, or religious elementary or secondary school from a 529 Plan. Distributions in excess of $10,000 are subject to tax. This limitation applies on a per-student basis, rather than a per-account basis.

Note: QTPs are also called 529 Plans because they are authorized under section 529 of the Internal Revenue Code.

- Coverdell Education Savings Accounts (ESAs). A Coverdell ESA can be used to pay a student’s eligible K-12 expenses, as well as higher education expenses. Coverdell ESA contributions are limited to $2,000 total per year for each beneficiary, no matter how many accounts have been established or how many people are contributing. Unless the beneficiary is a person with special needs, contributions to a Coverdell ESA must stop before the beneficiary reaches age 18 and the account balance must be distributed within 30 days after the beneficiary reaches age 30 (or dies, if earlier).

Exclusions From Gross Income

An exclusion from income means you do not report the benefit you receive as income and you do not pay tax on it, but you also cannot use that same tax-free benefit for a deduction or credit. • You may exclude the part of scholarships, fellowships, and grants that you use for qualifying education expenses while you are a degree candidate.

- You may exclude up to $5,250 paid for you under a qualifying educational assistance plan. Additional amounts are included in your W-2 income, unless they are a working condition fringe benefit. This includes principal or interest of any qualified education loan of the employee.

- If you cash in qualified U.S. Savings Bonds to pay for eligible education expenses for yourself, spouse, or your dependent, you may exclude the bond interest from income. Income limitations apply.