Which Tax-Filing Status Is Best? Should I Choose Single or Head of Household? Can You Claim Yourself as a Dependent?

Single

You can file as Single if any of the following was true on December 31, 2021.

- You were never married,

- You were legally separated, according to state law, under a final decree of divorce or separate maintenance. An interlocutory decree is not a final decree.

- Your spouse died before January 1, 2021, and you did not remarry in 2021.

If you meet the definition of unmarried, file as Single unless the requirements for one of the following filing statuses are met.

- Head of Household, or

- Qualifying Widow(er) with Dependent Child

Married Filing Jointly (MFJ)

You can file a joint return in 2021 with your spouse if:

- You were married at the end of 2021, even if you did not live with your spouse at the end of 2021.

- Your spouse died in 2021, and you did not remarry in 2021.

- You were married at the end of 2021, and your spouse died in 2022 before filing a 2021 return.

- You lived with a person in a common-law marriage recognized in the state where you live or in the state where the common-law marriage began.

You can file MFJ if both you and your spouse agree, otherwise you may file:

- Married Filing Separately (MFS), or

- Head of Household (HOH) if you meet the requirements to be “Considered Unmarried.”

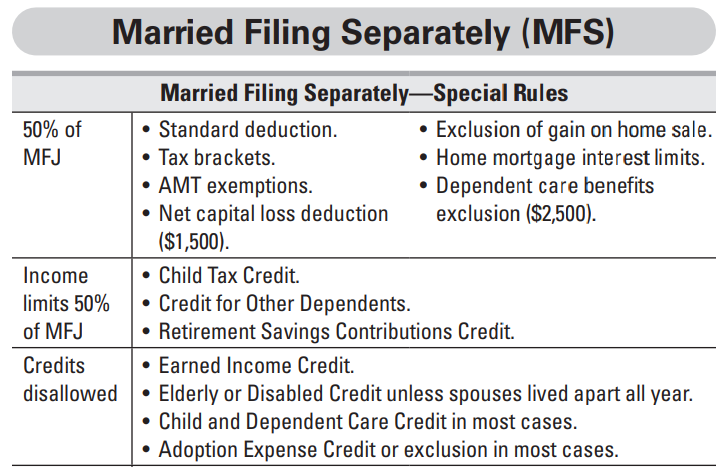

Any taxpayer that was married at the end of 2021 can file as MFS. Generally, you will pay more tax by filing an MFS.

Head Of Household (HOH)

The HOH filing status applies to unmarried individuals (or married individuals considered unmarried) who provide a home for a qualified individual.

Qualifying Child. The term qualifying child for purposes of the HOH rules has the same meaning as for the dependency test.

Qualifying Relative. A qualifying relative can be a qualifying person for HOH filing status if you paid more than half the cost of keeping up a home where the qualifying relative lived for more than half the year. You must be eligible to claim the qualifying relative as a dependent, and the qualifying relative must meet one of the following relationship tests.

- Son, daughter, stepchild, foster child, or a descendant of any of these (such as a grandchild),

- Brother, sister, half brother, half sister, or a son or daughter of either (such as a niece or nephew),

- Father, mother, or ancestor or sibling of either, (such as grandmother, grandfather, aunt, or uncle), or

- Stepbrother, stepsister, stepfather, stepmother, son in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law.

Note: A person other than the relationships listed above, who lived with you all year as a member of your household, can qualify as your dependent, but such a person who is a dependent only because they lived with you all year does not qualify you for HOH filing status.

Temporary Absences. Temporary absences for special circumstances count as time lived in your home. Special circumstances include time away from home going to school, vacation, business, medical care, military service, and detention in a juvenile facility. A person who was born or who died during the year is treated as living in the home for the entire year if the home was their main home for the part of the year he or she was alive.

Married Individuals Considered Unmarried. A married individual can be considered unmarried for HOH purposes if all the following apply.

- You lived apart from your spouse for the last six months of the year. Temporary absences for special circumstances, such as for business, medical care, school, or military service, count as time lived in the home.

- You do not file a joint return with your spouse.

- You paid over half the cost of keeping up the home during the year.

- Your home was the main home of your child, stepchild, or foster child for more than half the year.

- You claim this child as a dependent, or the child’s noncustodial parent claims him or her as a dependent under the rules for children of divorced or separated parents.

Qualifying Widow(Er) (QW)

The QW filing status is available for the first two years following the year your spouse dies, provided all the following requirements are met.

- Your spouse died in 2019 or 2020 and you did not remarry in 2021.

- You have a child or stepchild that you can claim as a dependent. This does not include a foster child.

- Your child lived in your home for all of 2021. If there is a temporary absence for special circumstances, the child is not considered to be away from home, such as for school, vacations, medical care, business, military service, or detention in a juvenile facility.

- You paid over half the cost of keeping up a home.

- You filed a joint return with your deceased spouse in the year of death or you could have filed a joint return that year.

If your spouse dies in 2021, you are married and can file a joint return for 2021 and you cannot file as a Qualifying Widow(er) until 2022.