Are Stocks and Bonds Tax Deductible? Can I Claim Financial Advisor Fees on My Tax Return? How Do I Avoid Capital Gains Tax on Mutual Funds?

Stocks, Bonds, And Mutual Funds

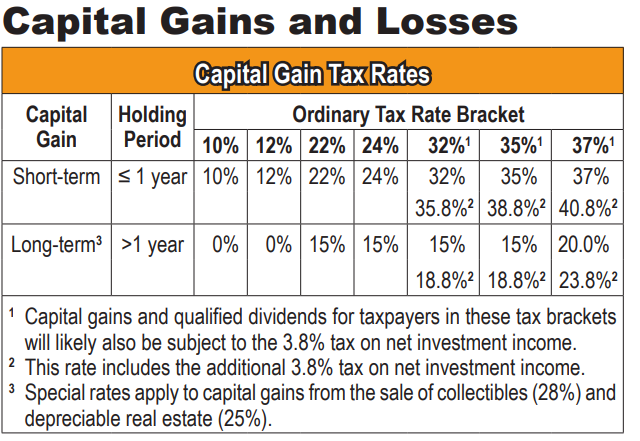

Capital Losses offset capital gains and, to the extent there is an excess loss, up to $3,000 ($1,500 MFS) can be deducted against ordinary income each year. Any remaining loss is carried forward indefinitely to future tax years.

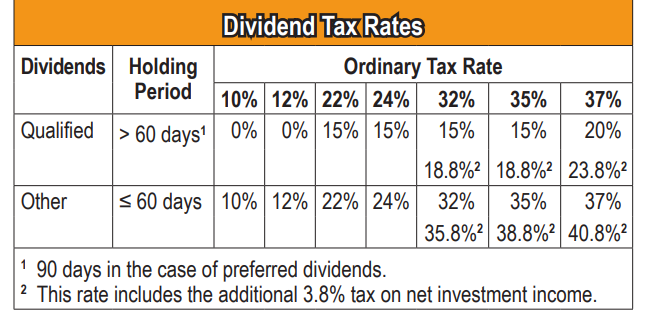

Qualified Dividends

Qualified Dividends are dividends received from domestic corporations and qualified foreign corporations. A taxpayer must hold the stock for more than 60 days (90 days for preferred stock) for the dividend tobe treated as a qualified dividend.

Stocks And Mutual Funds

Holding Period. The holding period for stocks traded on an established securities market and mutual fund shares begins on the day after the trade date and ends on the date sold (trade date).

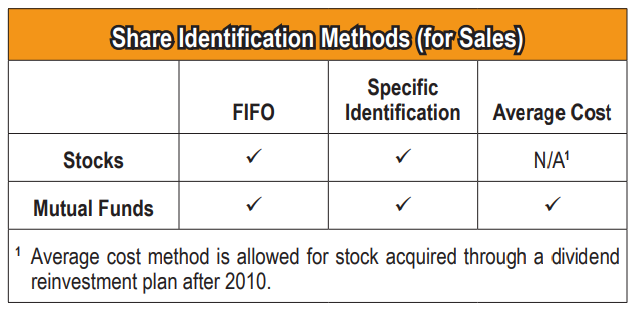

First-in, First-out (FIFO) Method. If the stock or securities have been acquired on different dates or at different prices, and the taxpayer does not or cannot identify the specific shares sold, they are considered to be sold in the order they were purchased.

Specific Identification Method. If the taxpayer specifically identifies the shares sold, the basis and holding period of those shares are used in computing the character (short-term or long-term) and amount of the gain or loss.

Average Basis Method. Each share’s basis is the total basis of all shares (in all accounts holding such shares at the time of the sale) divided by the number of shares. To determine holding period, the shares disposed of are considered to be those acquired first (FIFO method).

Worthless Securities

A taxpayer is allowed a capital loss for securities held as an investment if the securities become worthless. The loss is allowed only in the year the stock or security becomes completely worthless; partial losses are not allowed. Worthless securities are treated as though they were sold on the last day of the tax year. This deemed date of sale is used to determine if the loss is long-term or short-term.

Wash Sales

A wash sale occurs if a taxpayer sells or trades stock or securities at a loss and within 30 days before or after the sale, directly or indirectly:

1) Buys substantially identical stock or securities,

2) Acquires substantially identical stock or securities in a fully taxable trade or

3) Acquires a contract or option to buy substantially identical stock or securities.

If the wash sale rules apply, the loss is deferred and the basis of the new shares is adjusted accordingly.

Caution: Taxpayers must consider activity in their

IRAs and other retirement accounts when applying

the wash sale rules to their taxable accounts (that is,

purchasing a security in an IRA can result in a wash

sale in a taxable account).