Are Divorce Settlements Subject to Tax? Is Lump Sum Alimony Taxable in 2021? Is a Property Settlement Taxable?

Divorce Property Settlements

- The transfer of property between divorcing spouses is tax-free whether it is marital or separately owned property, provided it occurs 1) within one year after the date the marriage ends or 2) within six years if the transfer is made pursuant to a written property settlement.

- The transfer is tax-free even if property is encumbered by liabilities that exceed the property’s basis.

- Neither spouse recognizes gain or loss even if one spouse pays the other spouse for the property.

- Tax basis and holding period transfer with the property.

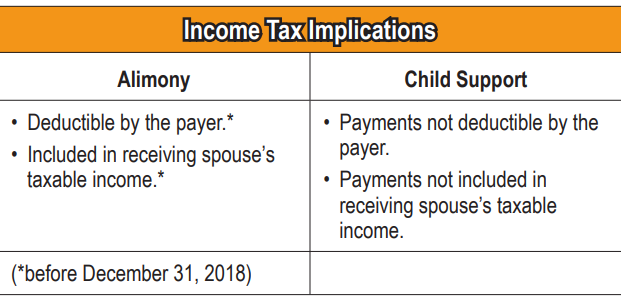

Alimony And Child Support

Characteristics of Alimony

- Payments must be made after a written agreement is executed.

- Payments may not be greater than the amount designated in a written

agreement.

- Payments may not be clearly associated with a child contingency.

- Payments cannot continue after death of spouse.

- Written agreement cannot state that payments are not alimony

Recapturing Excess Alimony Payments

- Recapture can only occur in the third post-separation year.

- Recapture causes the payer’s excess alimony deductions in one year to be included as taxable income in a subsequent year.

- Recapture causes the recipient’s excess taxable income in one year to be deducted in a subsequent year.

- Excess second-year payments are those that exceed the third-year payment by more than $15,000.

- Excess first-year payments are those that exceed the sum of (1) $15,000 plus (2) the average of the unrecaptured second-year payments plus the third year payments.

Dividing Retirement Accounts

Employer Qualified Plans

- Subject to qualified domestic relations orders (QDROs).

QDRO Limitations:

- Cannot provide increased benefits.

- Cannot override another QDRO.

- Cannot require a different benefit or option that is not otherwise provided in the plan.

QDRO Tax Effects:

- Benefits paid to a plan participant’s child or dependent are treated as paid to the participant.

- Benefits paid to a plan participant’s spouse or former spouse are included in the spouse’s income.

- The 10% early distribution penalty does not apply to distributions under a QDRO.

Individual Retirement Arrangements (IRAs)

- Not subject to qualified domestic relations orders (QDROs).

Tax Effects Of Transfer:

- Transfer to a spouse or former spouse is not a taxable event to either spouse if required by the divorce decree or separation agreement.

- a 10% early distribution penalty may apply to the receiving spouse who makes a withdrawal from transferred IRA before age 591/2.

Transfer Methods:

- Change the name on the IRA.

- Direct trustee-to-trustee transfer of IRA assets.

Tax Filing In Year Of Divorce

- In the year divorce is final, spouses no longer eligible for married filing jointly status (unless remarried by year-end).

- Each spouse’s income and deductions through the date of divorce depend on domicile—community property state or non-community property state.

Community Property States

- Former spouses report their share of community income and deductions up to the time the divorce is final.

- Spouses report their separate income and deductions for the remainder of the year.

- Federal income tax withholding associated with community income is split between the spouses in the same manner as the income.

- Joint estimated tax payments may be split between the spouses in any manner agreeable to both.

Non-community Property States

- Earned income is taxable to the person who earned it.

- Income from property is taxable to the property’s owner.

- Income from jointly owned property is usually taxed 50% to each joint owner.

- Deductions paid with separately owned funds generally go to the spouse who paid them.

- Deductions paid out of a jointly owned account are presumed to be paid half by each spouse.

- Federal income tax withholding reported by the person who earned the income.

- Joint estimated tax payments may be split between the spouses in any manner agreeable to both.

Legal And Accounting Fees

Legal, accounting and other professional fees paid in connection with obtaining a divorce are generally not deductible. The following exceptions are listed below for tax years 2017 and earlier. This was removed for tax years 2018 and later. The following expenses are deductible as itemized deductions subject to the 2%-of-adjusted gross income (AGI) floor:

- Expenses related to obtaining or maintaining taxable alimony.

- The cost of obtaining professional advice on the tax effects of an agreement dealing with alimony, child support or a property settlement.

Even if legal or other professional fees are not deductible, it may be possible to obtain an indirect deduction by adding them to the basis of assets. An asset’s tax basis can be increased by any portion of the fees allocable to defending the taxpayer’s title to the asset.